Straddle Strategy Explained: Types, Benefits, Risks, and Use Cases for HNI Investors

Introduction

Often, traders assume the market will follow a certain direction — bullish or bearish. But, at times, you're confident a big move is coming, but have no idea which way it'll go.

For High Net-Worth Individuals (HNIs) managing large portfolios, this matters.

Budget announcements, RBI policy decisions, US Fed meetings, geopolitical escalations, or events where big moves are almost certain, but the direction is a coin flip.

That’s where the “Straddle Option Strategy” sounds relevant!

Stay tuned as we explore what the straddle option strategy is, its types, mechanism, why HNIs see it as a leverage, and key risks to consider before implementing it.

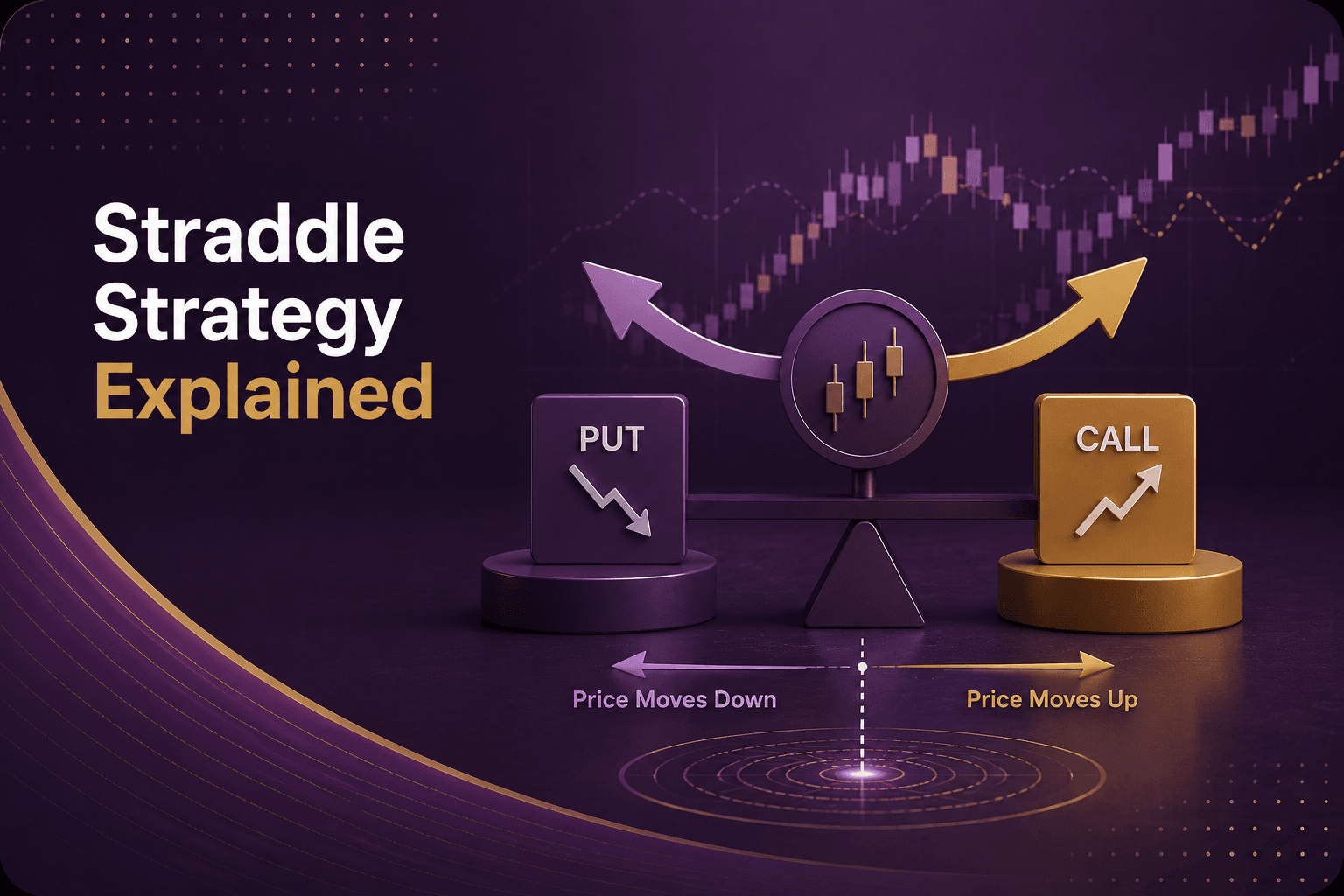

What is the Straddle Option Strategy?

In stock market, Straddle is an options strategy to buy (or sell) a call and a put option of the same underlying asset;

At the same strike price

With the same expiry date.

In dictionary words, the term "straddle" literally means standing with one foot on each side. So, while you're straddling, the straddle strategy positions the current price to profit whether it moves up or down.

Understand it in this way:

A call option makes money when prices go up. A put option makes money when prices go down. When you buy both at the same time and at the same price, you're covered in both directions.

That’s what the Straddle Option Strategy is all about.

How Does the Straddle Strategy Work?

A straddle strategy works by pairing two at-the-money options (a call and a put) at the same strike price and expiry. So any large price movement in either direction may be a win-win, while the maximum loss is limited to the total premium paid.

Example

Let's walk through a real example of Straddle strategy on Nifty.

Assume, Nifty is trading at 24,000.

Mr.A buys

1 Nifty 24,000 Call (CE) at a premium of ₹150 per unit

1 Nifty 24,000 Put (PE) at a premium of ₹150 per unit

Total premium paid = ₹300

Now here's what happens at expiry:

If Nifty rises to 24,500:

If Nifty falls to 23,400

If Nifty stays at 24,000

Your call gains are ₹500 per unit. Your put expires worthless.

Net profit = (₹500 – ₹300) × 50 = ₹10,000.

Your put gains are ₹600 per unit, but your call expires worthless.

Net profit = (₹600 – ₹300) × 50 = ₹15,000.

In this case, both options expire worthless, and you lose the entire premium.

Benefits of the Straddle Strategy

The straddle strategy offers four distinct advantages that make it particularly useful for HNI investors managing event-driven risk across large portfolios.

No Directional Bias Needed - HNI investors don't need to predict whether the market will go up or down, only that it will move significantly. This is useful during uncertain events like elections, geopolitical escalations, or surprise policy announcements.

Defined Maximum Loss - In a long straddle, your worst-case scenario is losing the premium paid. For HNI investors sizing positions in lakhs, knowing your maximum downside in advance is essential for portfolio risk management.

Works In Both Directions - Whether the market crashes or rallies, one leg of the straddle profits. This symmetry is a feature of straddle, compared to options strategies.

Captures Volatility Expansion - Even before expiry, if implied volatility rises sharply (say, India VIX spikes from 12 to 18), both your call and put premiums increase in value. This gives investors an exit at a profit without the underlying price moving at all.

Types of Straddle Strategies

There are two primary types of straddle strategies: Long straddle, where you buy both options and profit from large moves, and the short straddle, where you sell both options and profit from the market staying flat.

Let us understand them in detail:

1. Long Straddle (buying both options)

When you expect the market to move sharply (either up or down), the long straddle strategy helps. Here, you buy a call and a put at the same strike price and expiry.

Basically, buying two options means you pay the premium upfront. Hence, the risk is limited to the total premium paid.

2. Short Straddle (selling both options)

A short straddle is used when you expect the market to remain relatively stable and not make any significant move before the options expire.

In this strategy, you sell both a call option and a put option with the same strike price and expiry date.

Since you are selling the options, you receive the premiums upfront. So, even if both options to expire worthless, you still get to keep the entire premium collected as profit.

Key Differences: Long Straddle vs Short Straddle

Here’s the key difference between a long straddle and a short straddle:

| Long Straddle | Short Straddle |

Market Expectation | High volatility | Low volatility |

Position | Buy call + buy put | Sell call + sell put |

Premium | Paid upfront | Received upfront |

Maximum Profit | Potentially significant | Limited to the premium received |

Maximum Loss | Limited to premium paid | Can be substantial |

Suited when? | Expecting large price swings | Expecting a range-bound market |

How Do HNI Investors Use Straddle Strategies?

HNI investors use straddle strategies because they manage large, diversified portfolios that face concentrated event risk. And straddle allow them to hedge from volatility without taking a directional view on the market.

Here's why straddles are particularly relevant for HNI portfolios:

Portfolio hedging around events - Using the straddle technique acts as an insurance for HNIs to offset portfolio losses on one side while capturing gains on the other.

Capital efficiency - A straddle requires only the premium amount as upfront capital (plus applicable margins). And for an HNI, deploying a safety amount in a straddle to protect their crore portfolio is a small, well-defined cost.

Volatility as an asset class - Experienced HNI investors and family offices treat volatility itself as an investable theme. With the straddle option strategy, it is possible to leverage volatility and protect from uncertainty.

(Note: Please consult a SEBI-registered investment advisor before making any trading or investment decisions.)

Key Considerations Before Implementing a Straddle Strategy

Before placing a straddle trade, consider implied volatility at entry, time decay exposure, event timing, and other factors to use this strategy effectively.

Let us look at each in-depth:

1. Implied volatility (IV) at entry

If implied volatility is already elevated when you buy a straddle, the premiums are inflated. It means the market needs to move even more to justify the cost.

2. Time decay (Theta)

Options lose value every day. So, the closer you get to expiry without a significant price swing, the faster your premiums erode. One such example is a long straddle that bleeds more money if the market doesn't move.

3. Exit discipline

Setting a predefined exit plan tries to avoid emotional decisions. It sets clear profit targets and stop-loss levels before entering the trade.

4. Liquidity

Choose options with high trading volumes and tight bid-ask spreads. Better liquidity makes it easier to enter and exit positions efficiently.

5. Position sizing

Avoid allocating too much capital to a single straddle trade. Proper position sizing helps manage risk and limit potential losses.

Conclusion

For HNI investors, a straddle is a tool for event-driven hedging, portfolio insurance, and the ability to tackle uncertainty. All three things matter more as portfolio size grows.

But it's not a free lunch. You're paying a premium for the privilege of being positioned on both sides. If the market doesn't move enough, you lose that premium entirely.

Hence, consulting a financial advisor before implementing the strategy can help position your portfolio better.

Frequently Asked Questions

What is a straddle strategy in options trading?

A straddle strategy involves buying (or selling) a call option and a put option at the same strike price and expiry date on the same underlying asset.

What is the difference between a long straddle and a short straddle?

How are gains from the straddle option strategy taxed in India?

Disclaimer

The information provided in this article is for educational and informational purposes only. Any financial figures, calculations, or projections shared are solely intended to illustrate concepts and should not be construed as investment advice. All scenarios mentioned are hypothetical and are used only for explanatory purposes. The content is based on information obtained from credible and publicly available sources. We do not guarantee the completeness, accuracy, or reliability of the data presented. Any references to the performance of indices, stocks, or financial products are purely illustrative and do not represent actual or future results. Actual investor experience may vary. Investors are advised to carefully read the scheme/product offering information document before making any decisions. Readers are advised to consult with a certified financial advisor before making any investment decisions. Neither the author nor the publishing entity shall be held responsible for any loss or liability arising from the use of this information.